January 7, 2018 – The labor market ended 2017 with December payroll growth of 148,000, below expectations of 193,000 but a respectable showing nonetheless. A similar monthly pace in 2018 would be enough to push the unemployment rate, which stayed at 4.1% in December, below 4%. During the fourth quarter, the U.S. economy created 612,000 jobs, bringing the total for 2017 as a whole to 2.1 million. Wages grew 0.3% in December but just 2.5% over the past 12 months. The latest payroll data supports the Fed’s intended path to gradually raising rates in 2018. Expectations remain firm the Fed will lift rates three times in 2018 with the first hike expected in March where market-implied odds remain at 79% for the Fed to act.

Looking back on the equity, rate and credit markets of 2017, the S&P 500 index notched 62 record-high closes for a 21.83% overall gain. More surprisingly, en route to that gain, the index provided a positive return in every month of the year for the first time ever, without a single correction of 5% or more. In fact, there were just eight days in which the S&P 500 rose or fell by 1% or more in a single trading session. On a daily basis, the index rose or fell by 0.50% or less 80% of the time. Treasury yields finished the year at 2.40% as measured by the 10 year Treasury after starting 2017 at 2.42%. While the 10 year Treasury hardly moved over the course of the year, 2 year Treasuries rose 70 basis points causing the yield curve, as measured by the spread between 2 and 10 year treasuries, to flatten to a spread of 50 basis points, the lowest spread in the last 10 years. The Fed’s tightening in 2017 and expected tightening in 2018 and beyond are responsible for much of the flattening. Investment grade corporate credit spreads and high yield credit spreads tightened roughly 46 basis points over the year as cash rich investors needed to put money to work. Looking forward, the recently passed corporate tax cuts will fuel optimism about 2018 earnings and could provide a further lift to equities and a further tightening of credit spreads. Additionally it will be important to watch for signs of inflation, which to date have been absent, and monitor labor force participation. More expansion of the labor force will reduce wage pressure enabling the Fed to raise rates more slowly. However, should the labor force not increase, we could finally see more wage growth encouraging the Fed to tighten more aggressively over time.

For Alternative Lenders, 2017 was the perfect environment of continued low rates, tight credit spreads, low volatility and strong investor appetite for risk adjusted assets resulting in continued growth for platforms. So far, 2018 is starting out as a continuation of that theme. Consumer lender and personal finance company MoneyLion announced that it has raised a $42 million Series B funding round led by existing investor Edison Partners, with participation from other existing investors including Fintech Collective, Grupo Sura, as well as new investors Greenspring Associates and Danhua Capital. Small business lender Funding Circle, and INTRUST Bank, a regional bank headquartered in Kansas, announced that INTRUST will begin funding U.S. small business loans originated through Funding Circle. Look for a very active 2018 in the Alternative Lending space.

Opinions expressed within the commentary are general opinions of Chris Lalli and are not opinions of CapAccel. Nothing in this commentary should be viewed as solicitation to buy or sell specific securities or a recommendation to participate in any transactions.

Sources: TIAA-CREF, Wall Street Journal, PeeriQ

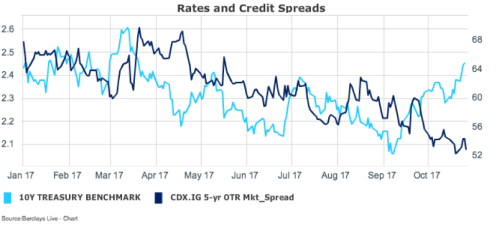

Credit spreads, as measured by Markit’s Investment Grade 5 year credit default swaps spread index, continue to tighten as growth picks up and corporate earnings remain strong. For Alternative Lenders, continued low rates and tight credits enable a robust lending environment.

Credit spreads, as measured by Markit’s Investment Grade 5 year credit default swaps spread index, continue to tighten as growth picks up and corporate earnings remain strong. For Alternative Lenders, continued low rates and tight credits enable a robust lending environment.